How Much is Too Much Income to Qualify for Financial Aid?

By Ian Aguilar

Financial aid is utilized by about two-thirds of full-time students each year through the forms of grants and scholarships, and yet only 75% of families actually fill out the necessary FAFSA (Free Application for Federal Student Aid) forms to garner that money. The most common answer as to why parents and students didn’t is that they felt they wouldn’t qualify for any aid. Sadly, there are a lot of people who fall victim to this assumption and leave free money on the table that could otherwise go towards reducing the price of college tuition.

Income is the quickest way that someone will typically disqualify themselves out of financial aid, but at what point does that happen? To answer this question let's first try and understand exactly how financial aid is calculated. Plainly put the amount of financial aid that someone qualifies for when looking at any specific school is determined by two main variables; the quoted cost of attendance to that school (including tuition, fees, room & board, books, etc.), and your families EFC (Expected Family Contribution), which is calculated by a standard federal formula.

COA (cost of attendance) – EFC (expected family contribution) = Financial Aid Qualification

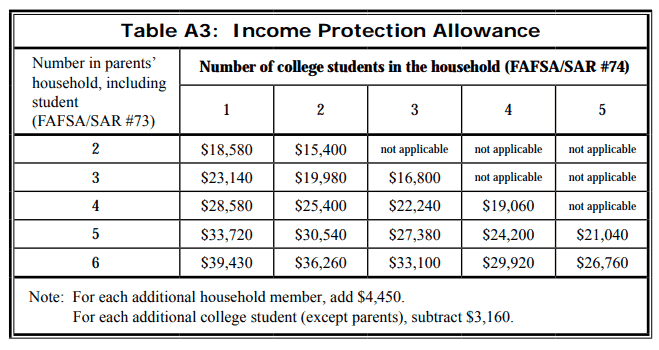

So how does income play into all of this? It tends to be the variable that most drastically affects your EFC calculation. A large percentage of parents' "discretionary" income, anywhere in the range of 22% to 47%, is taken into account towards your EFC. There is an amount of the parent's income that is not taken into account ranging from $18,580 to $39,430 (refer to Table A3 below) which depends on the total amount of kids and how many of them are in college. Once income goes beyond those allowances it starts lowering your financial aid qualification.

Here are a few rough guidelines that can help you understand how your total income will affect aid:

For any amount above your income protection allowance, roughly every $10,000 in extra income lowers your financial aid qualification by another $3,000.

Once the income is above $100K roughly 1/5th to 1/4th of income will be counted towards your EFC. As your income increases that fraction of your income also increases and can even creep towards 1/3rd or more.

With only one child attending college normally an income above $125K will disqualify you from financial aid qualification at a public university, and about double that, or $250K in income will disqualify you from garnering financial aid.

IMPACT OF FAMILY SIZE ON FINANCIAL AID

Another very important aspect to note is that if you have multiple kids attending school at the same time, then you as a parent can split your EFC number between each of your children. So, if your EFC was $30,000, however, another one of your children began attending college, their respective EFC numbers would now be $15,000. If you didn’t qualify for financial aid before your other child went to college, it may make sense to apply again now that you have more kids in college.

HIGHER TUITION IS BETTER FOR THE EFC

The other factor in this equation that will allow you to make more money while still qualifying for financial aid is the cost of attendance at the school that you are applying to. If you are applying for a school that has a cost of $65,000 versus a school that costs $25,000 you can make a lot more money and still qualify for financial aid at the more expensive school, where the cheaper school may not grant you any.

MIND THE DETAILS

Another factor that is very important to note the timing of income received. Income on the financial aid form is pulled from the prior-prior year to the filing. So, a student attending their first year of college in the fall of 2019 would have to use their parent's income from their 2017 tax filings.

The mismatch of timing grants people the ability to purposely receive bonuses, inheritances, retirement plan distributions, and even capital gains distributions in certain years to maximize their ability to qualify for financial aid. So be sure to avoid any artificial increases in income that can negatively impact financial aid. You can attempt to delay receipt of those incomes or offset gains with losses as a couple ways to defray the effect of extra income on financial aid.

Once your child is beyond the second semester of their sophomore year income received becomes irrelevant to their financial aid, but be aware of how it may affect younger children if you have any. In order to illustrate some of these principles, we’ve laid out a simple example.

Example:

A couple living with two kids makes $162,000 per year. Their oldest is in college finishing his freshman year and currently doesn’t receive any financial aid going to a school that has a cost of attendance of $30,000. Their second child is a rising junior and looking at attending a school with the cost of attendance of $60,000. The oldest in his first two years of college didn’t receive any financial aid because of the following:

$30,000 (cost of attendance) – (¼ * $162,000 = $40,500) = -$10,500 (financial aid qualification)

The EFC estimate is purely based on income and no other assets. This is purely an estimate using the general rule of thumb stated earlier. Now when the second child is going off to college if we go through the same exercise for both kids the financial aid qualification comes out positive:

Child 1

$30,000 (cost of attendance) – (¼ * $162,000 = $40,500/2= $20,250) = $9,750

(financial aid qualification)

Child 2

$60,000 (cost of attendance) – (¼ * $162,000 = $40,500/2= $20,250) = $39,750 (financial aid qualification)

Here we can see how not only more kids in college can help qualify for more financial aid, but how the cost of the school selected can greatly alter your financial aid qualification. A family that previously didn’t qualify for any financial aid with their first child in college by himself, now qualify for up to $48,950 between their two children. Their income limited them initially, but this showcases how much certain factors can alter the idea that their income excluded this family from qualifying for financial aid.

If this couple was expecting a large bonus payment, let's say in the realm of $30,000 in the current year, I'd suggest they delay their bonus to the following year if possible to ensure that their oldest child can still qualify for financial aid. Utilizing the rule of thumb stated earlier a bonus of that size could eliminate around $9,000 ($30,000 X .3) worth of financial aid.

BIGGEST TAKEAWAY

The easiest way to tell “when do I make too much” is by taking the total cost of attendance between the schools your kids are attending and seeing if 1/4 of your income is greater than that amount. In the example above the total cost of attendance for the two children is $90,000 (30,000 + 60,000). So someone who has a $360,000 income (4 X 90,000) is likely making too much money to explore any financial aid strategies.

Once you’re above and beyond that mark then it may be time to look towards other strategies to aid with the net cost of college. Understanding that along with the fact that it's important to always apply for financial aid even if you are beyond those amounts is critical. Life circumstances can change on a dime, so ensuring that you filled out the necessary forms can leave the door open to receiving aid, should your financial situation change.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Paragon Wealth Strategies, LLC [“Paragon”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Paragon. Please remember that if you are a Paragon client, it remains your responsibility to advise Paragon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Paragon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Paragon’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.wealthguards.com. Please Note: Paragon does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Paragon’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Also Note: IF you are a Paragon client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.